Sounds courtesy of Sound Bible, Music Courtesy of bensound.com

Evergreen Mortgage’s Guide to Christmas Budgeting

© Copyright Christine Matthews and licensed for reuse under this Creative Commons Licence.

Christmas is just around the corner folks! For many this is a time of joy, where families come together to exchange gifts and enjoy one another’s company.

However, Christmas can also be a budget-buster. The average American household plans to spend just under $1000 this year on Christmas gifts, and few of us have enough discretionary monthly income to cover that. If you’re just now having the Christmas budget discussion, the reality is, it’s a bit late.

Many will use credit cards to finance the holiday cheer, some may turn to crime, and the Flanders will have an “Imagination Christmas” (Simpsons, anyone?), but once the tinsel settled, here is how to prepare for next Christmas.

Warning: Budgeting for Christmas is just like budgeting for anything else. This is going to be a general budgeting lecture, not just a Christmas post, so if the discussion of budgeting turns your stomach, beware.

Amortize the Expense

“Amortization” is one of our favorite terms in the mortgage industry. It simply means to take a single expense and break it up into increments, or payments. Amortize your projected 2017 Christmas expenses (let’s say, $1000) by figuring out your “monthly” Christmas expense; $1000 / 12 = $83. So, you’ll need to set aside $83/month in 2017 to pay for Christmas. Now, let’s work this into the rest of your budget.

Create a list of expenses

First, write down what your different expenses are and list them by category in order of importance: Mortgage/Rent, food, kids clothing, forecasted repair costs, auto-loans, student-loans, taxes, emergency savings, and any costs that are absolutely necessary. It’s helpful to see what your expenses in these categories were for the previous year, so that you know what to plan for.

Next, create a list of “less necessary costs” such as a planned vacation, optional upgrades on home and vehicles, Christmas(!), etc.

This can be a moment of reckoning for many of us. If you find that your expenses are outpacing your income, then it’s time to start trimming expenses or find a feasible way to increase your income, or both.

Automated Payments and “Buckets”

Budgeting is all about discipline, and one of the keys to successful budgeting is to do whatever is feasible to reduce temptation. Just as someone who is dieting would find it unwise to leave a jar of cookies on the counter, a budgeter needs to make sure spoken-for funds are “off limits”. This is best done with automated payments/transfers and “buckets”.

Automatic Payments/Transfers: For set monthly expenses (like your rent/mortgage, car payment, etc.), set up automatic payments and get the money out of your account as fast as possible. This will keep you from making late payments, but also keep you from thinking you have more discretionary income than you really do. Automate as much as you can!

Buckets: For your non-monthly expenses (like Christmas), have a savings account set up (you can use more than one account, but that can get cumbersome) and automatically transfer into that account the amount needed to cover the monthly portion of those expenses. For example, if you were setting aside $83/month for Christmas, $50/month for an upcoming vacation, and $200/month for a tuition bill, then your monthly “bucket” transfer would be $333. Use a spreadsheet or ledger to keep track of how much is in each bucket. Make this bucket account as inaccessible as possible (you don’t want it to be “easy” to blow your budget!).

The leftover money can be your “fun” bucket, money to play with and do as you please, eat-out, go to a ball-game, etc. As long as you have your necessary expenses covered, you won’t have to worry about coming up short later.

Enjoy the Christmas Season

It is a rather simple approach to saving and budgeting, but if you follow this key bit of advice, you won’t have to worry about not having enough come Christmastime, and you won’t fall short during the rest of the year either.

Again, this is all about discipline, and most of us will have to make some cuts/trade-offs to be successful budgeters, but as we’ve learned from the Rolling Stones; “you can’t always get what you want, but if you try sometimes, you just might find, you get what you need.”

VA Loans: Reason Enough for Everyone to Join the Military

Image courtesy of Pixbay (https://pixabay.com/en/soldiers-military-attention-salute-559761/)

In my years of helping clients with their mortgages, I have been increasingly convinced of the superiority of the VA Loan program (for those who can take advantage of it). I’m also surprised by how many borrowers don’t know they can take advantage of it.

Here are some of the key features/benefits of VA Loans:

No Down Payment

VA Loans allow a borrower to purchase a home without a down payment, with no penalty for doing so. There are other no-down-payment mortgage programs out there, but the interest rates and terms are normally significantly worse than normal loans. With VA Loans, the borrower is not penalized (as in a higher interest rate, reduced purchase price, etc.).

Refinance Implications: In the case of a refinance, a borrower can borrow the entire value of the home (again, with no penalties/negative consequences). This is especially helpful if a client wants to access the equity in their home (called a “cash-out refinance”), because they can take out far more than an FHA or Conventional loan.

No Mortgage Insurance

With Conventional loans, mortgage insurance is required any time the down payment is less than 20%. For FHA, mortgage insurance is always required. VA Loans do not carry mortgage insurance, regardless of the size of the down payment. You can purchase/refinance up to 100% LTV (Loan to Value ratio) without wasting money on mortgage insurance.

Lower Rates and Higher Loan Amounts

VA Loan interest rates are typically less than Conventional mortgage rates and about equal to FHA rates, but without the mortgage insurance. VA Loans are also normally not subject to loan amount caps (Conventional and FHA loans are), allowing a client to purchase a larger home or cash out more equity. They also allow for higher debt-to-income ratios (similar to FHA), which lets borrowers qualify with a higher mortgage payment (and therefore, a larger home), than Conventional mortgages.

Less Strict Credit Requirements

VA Loans allow for lower credit scores (like FHA loans) and are more forgiving of significant negative credit events (like a bankruptcy). While Conventional and FHA loans have required waiting periods that have to pass before a borrower can get a new mortgage, VA Loans do not have set limits, allowing borrowers to qualify for a mortgage sooner (as long as the borrower is otherwise well-qualified).

You Don’t Have to be an Actual Veteran

A common misconception is that a former military member has to have fought in a war to qualify for a VA Loan. This is not at all the case; even time spent in the National Guard or Reserves will allow you to qualify for a VA Loan. There are several different qualification requirements, but essentially; as long as you finished your “stint” and weren’t dishonorably discharged, you should qualify for a VA Loan.

Want to see if you’d qualify for a VA Loan? We can quickly check your VA Eligibility as well as your capacity to buy a home/refinance.

Retiring a Millionaire: Why Owning a Home is King

Image by UnSplash

Becoming a millionaire is the quintessential American dream. While seemingly lofty, it is an achievable goal (there are about 11 million millionaires in the US as of 2011) and it is accomplished in a variety of ways: most people save it, many invest it, some start successful businesses, some buy the right scratch-off, Bernie Madoff steals it, etc., but we’re going to briefly discuss the most reliable, least labor-intensive, and most boring way of becoming one of the 2.5-Percenters: owning a home.

The reason that homeownership is such a beautifully simple and inexpensive way to wealth is because housing costs are required living expenses (unless you are happy living in mom’s basement and she’s nice enough to let you stay there for free). You have to eat, you have to sleep and wear clothes (please), and you have to have a roof over your head.

You’ve got 2 housing options: rent or own. Renting provides no return on investment. The rent you pay is like credit card interest: aside from giving you a month’s reprieve from the landlord, there is nothing to show for it in the end. Owning (assuming you pay a mortgage instead of a rent payment) leaves you with something: a house. Add to that the predictable nature of housing prices to rise and you have the recipe for millionaire-ship.

Example:

Homeowner Joe buys a modest house for $254,000 in Salt Lake City (the average home price these days). He puts down 5% and his total mortgage payment is about $1300 (which is significantly less than rent for that same home in Salt Lake). It’s a 30-yr mortgage and he doesn’t refinance (for simplicity’s sake) for the life of the loan (the next 30 years).

Joe has a relatively hard life for the next 30 years. His income is limited and he is never able to set aside anything for retirement (like an IRA). Nor does he work for a company that offers a 401K. In short, Joe has nothing to expect in the way of retirement income (except Social Security).

But, Joe is a millionaire.

Over the last 30 years, Joe has slowly chipped away at his mortgage. Bit by bit each month, the home becomes “his”. Also, the price of his home increases by an average of 4.00% each year (100-yr average and a modest estimate for Salt Lake). When Joe finally does retire at age 65, his mortgage balance is “0” and his home is worth $1,002,000.

And because math hasn’t changed since you’ve been in 1st grade: $1,002,000 - $0 = $1,002,000!

Joe can keep his home (his housing expenses will be cheap since he has no mortgage), rent it out, or sell it and rent a condo in Florida (just as rest stop for his constant travels). That $1,000,000 could equate to $6000/month in income for the next 20 years (if put in a conservative annuity).

Or he could convert it to nickels, buy an old empty swimming pool, and go swimming in his own “Money Bin”. Every day.

Notes/Disclaimers

We are huge proponents of diversification, especially IRAs and 401Ks. If Joe did have a 401K and they matched his contributions, putting aside just $150/month would give him another $600,000 at retirement.

Also, poop happens, and Joe/you may have to refinance at some point to cover unexpected medical expenses, job losses, divorce, etc. You may find yourself approaching retirement and still having 15 years on your mortgage. The point is that if you are a homeowner, you at least have the option of doing those things! Renters can’t cash-out equity to pay for medical bills because there is no equity. Even if your home isn’t paid off at retirement, you still have the equity (the difference between the home’s value and the balance of your mortgage) which could be substantial.

Call Evergreen Mortgage today. We’ll come to you to discuss your home-buying options.

Or buy more scratch-offs.

Evergreen's Guide: Skipping Mortgage Payments

Skipping 1 or 2 mortgage payments is an added benefit of refinancing. The additional cash can be a welcome contribution to your savings funds, retirement, etc. But the reasons and processes for skipping several mortgage payments is often misunderstood, so Evergreen Mortgage is here to dissipate the mists of darkness surrounding this concept.

Rate Post 9/2/2016

HOA’s: What to Expect and What to Watch For

What is an HOA?

If you purchase a condominium, townhouse, or property in a gated community or subdivision (anything considered a PUD, or a “Planned Unit Development”), you will likely be obligated to join that community’s Homeowners’ Association (HOA).

HOAs help protect property values and keep common areas/interests functioning properly. HOAs collect dues for the upkeep and management of common areas/interests such as insurance, security, landscaping, parks, parking lots, pools, security gates, pest control, etc. It’s important to note that “common areas”, at least for condominiums, often include anything not within the walls of your own unit, so HOA fees also cover the costs of maintaining (or replacing) roofs, exterior walls, stairwells, etc.

HOAs also set forth rules which may prohibit certain actions or activities such as painting your house neon green (thus lowering the value of not only your home, but the homes nearby); having a big, loud dog; parking in certain locations; or starting a garage band and playing at midnight. Typically the HOA can levy fines against individuals who break the rules and in some cases can even foreclose on your home.

Benefits of an HOA

The major benefit is from economies of scale. Because everyone is pitching in and the HOAs are buying these services in bulk, 50+ HOA members can negotiate better rates (per unit) than the individual homeowner. The overall cost is usually much cheaper for everyone involved. For example, the insurance that you would normally have to pay to protect your home from flooding, fires, or natural disasters –which normally cost you $40 – now costs $10 through the HOA.

These are typically things that a homeowner would naturally have to pay for anyway, so it is a major benefit to not only pay a bit less, but not have to worry about securing these services for yourself. (I.e. you don’t have to set-up trash pickup: it’s already available through the HOA.)

What to look for

It is important to read through the rules of the HOA (called the CC&Rs) to understand its responsibilities and what actions they are able to take in fulfilling those. Finding an HOA that lines up with your values is a must. Is garbage pickup included? What are the smoking restrictions? Are pets allowed (if you’re a big dog person, it might not be the best idea to jump into a community that forbids pet ownership)? What kind of insurance does the HOA have against flooding, fires, or other natural disasters? Is the HOA managed by professionals or by a few members? And finally, how much are the fees, and have they risen substantially in the last few years (and if so, why did they rise)?

Research what kind of reserves the HOA keeps. What sort of things do they spend it on: new roofs for homes or carnivals? Have they saved enough for upcoming maintenance or are they going to have to raise the dues? Try to find out if the HOA is spending their reserves on things that are truly important to you or things that you don’t really care about.

Finding out these key pieces of information can be a huge breath of relief – or a warning signal to stay away. Think seriously about whether or not you want to buy a home with the current HOA.

Conclusion:

All-in-all the benefits outweigh the costs. If you have a good HOA you can rest easy knowing that the neighborhood you bought property in will not only have its property value protected, but that the standards are clearly outlined for you to see up front. HOAs can save you a lot of time, money, and stress if managed properly.

Rate Post 8/15/16

Don't miss out on the opportunity to refinance into a lower rate if you haven't already done so. Additionally, it's a great time to upgrade your home, or even purchase a new one.

Rate Post 7/20/2016

Enjoy low rates through the summer!

Mortgage Definitions Made Easy

Whether you already have a mortgage, or are planning on purchasing a home, there are a lot of industry related terms that get thrown around rather casually. Here’s a handy guide for navigating through some of the lesser known terms.

Amortization

This simply refers to the schedule of how the loan is going to be repaid. For instance, you have both 15 year and 30 year fixed rate conventional loans. In the case of each of these, the amortization schedule would be the monthly payment for a 15 year, and 30 year respectively, including interest rates.

Closing Costs

These are costs associated with closing the loan which can include, but is not limited to: fees for a credit report, loan origination fees, and underwriting fees among others.

Mortgage Escrow

An escrow is the payment that is collected by the lender each month, along with the regularly scheduled mortgage payment, to pay for real estate taxes and hazard insurance premium. While mortgaged homeowners can choose to make these payments themselves, they often benefit from mortgage rate discounts by simply passing them on through the lender, who then holds the funds for payment to the homeowner’s county assessor and insurance company when the payments are due.

To find your home escrow payments, simply find your latest home real estate tax-bill, add in the annual insurance premium, and divide it by 12 (the number of months in a year) This is your monthly escrow payment.

PITI

This is an acronym which stands for Principal, Interest, Taxes, Insurance and represents the total housing payment made in that month. It is calculated by simply adding all of them together.

PMI (Private Mortgage Insurance)

When the loan to value ratio (LTV) is above 80% lenders will generally require private mortgage insurance (PMI) to guarantee the loan against default. Borrowers pay a monthly premium until the loan to value ratio (LTV) drops below 80%. In the case of FHA loans, the only way to get rid of PMI is to refinance into a conventional loan once the LTV is below 80%. Another popular option for conventional loans, to avoid having to pay the monthly mortgage insurance, is to take on a 2nd mortgage.

Points

Percentage points of the loan amount. As an option to borrowers, lenders can allow the borrower to “buy down” the interest rate by paying portions of the loan up front, saving the borrower money over the long term in the form of lower interest rates.

Title Insurance

Insurance paid by borrowers that ensure the property is free and clear of any liens against it, so that the property may be used as collateral in the event of a default on payment.

This is just a small list of terms that many individuals will often face when refinancing. For more information on terms like LTV, check out our video.

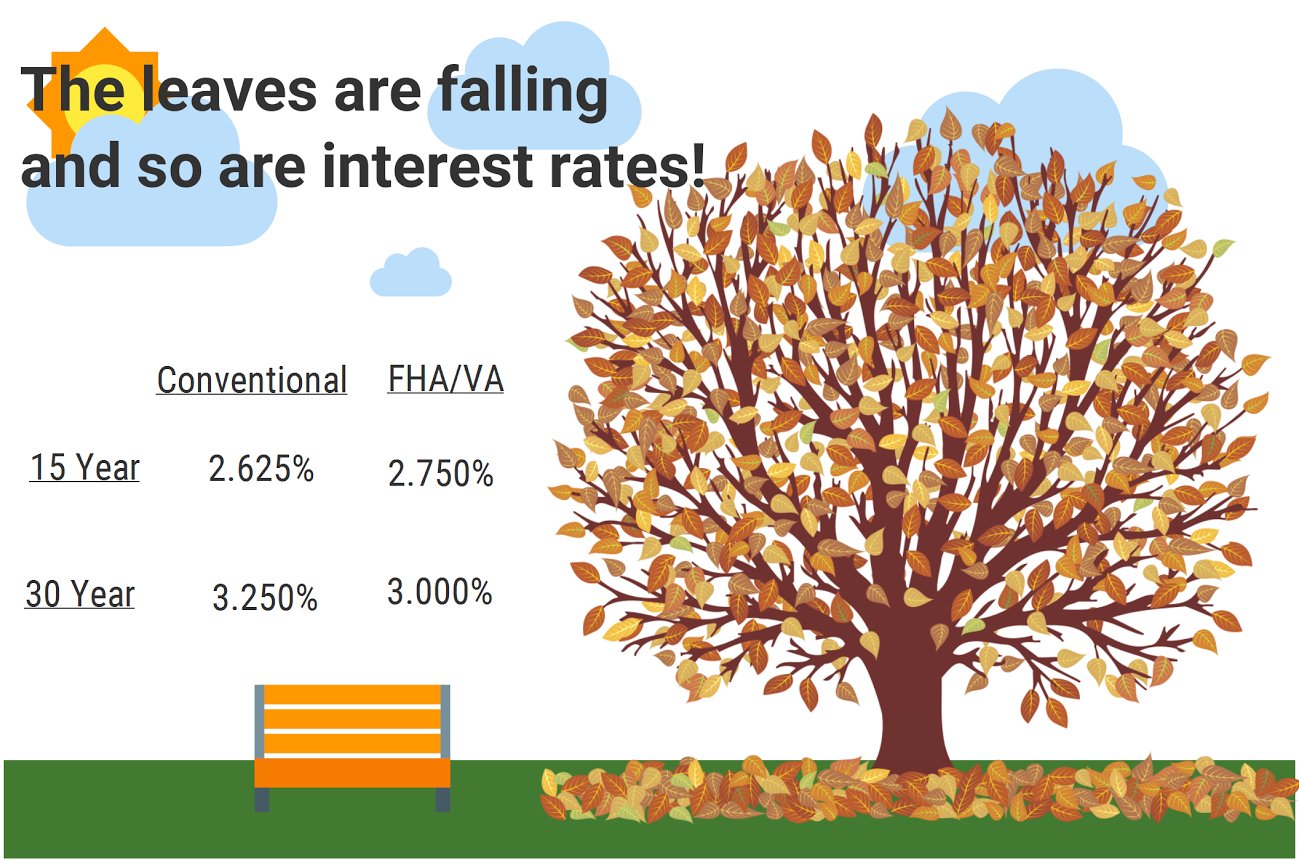

Rate Post 7/4/2016

No difference between 15 year conventional and 15 year VA!

Rentals An Excellent Investment if You Know What to Expect

If you’ve ever been a renter, you may at some point declared “dang, our landlord is making a killing on us!” and concluded that being a landlord is the key to wealth and power. While it may not be as glamorous as it is sometimes made to seem on infomercials and seminars, owning a home as a rental can be a significant portion of your wealth late in life, and more importantly, an excellent source of retirement income.

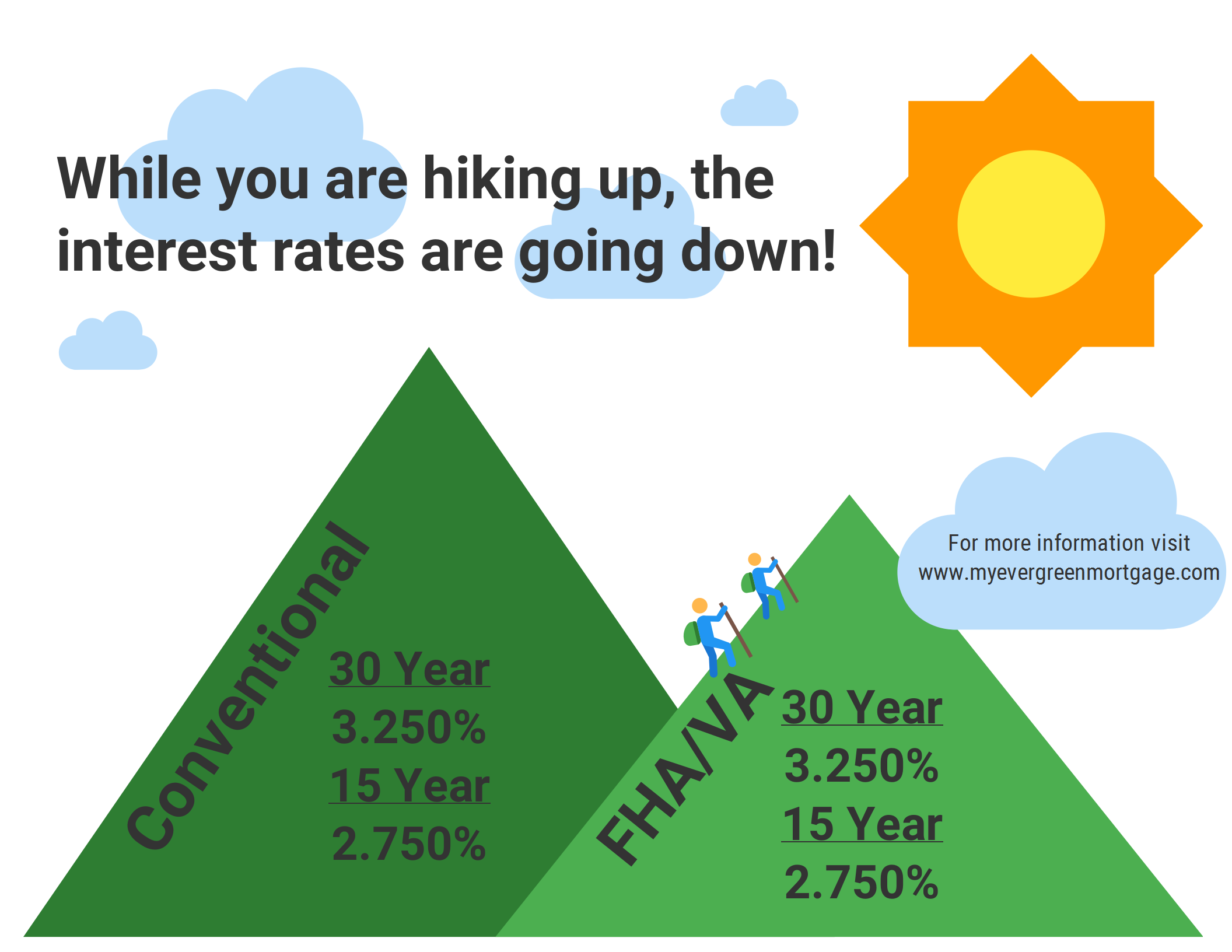

Rate Post 6/17/2016

Enjoy the lower rates through the summer!

Buying a Rental Property for Only 3.5% down How to Leverage Your Dear Children to Purchase Investment Properties for a Minimal down Payment

Normal Investment Property Requirements

Rental properties, if managed appropriately, are excellent investments and even one can significantly increase your income/assets in retirement. But, as is the case with most good investments, there are significant “barriers to entry”, particularly the down payment.

A primary residence (the home you live in) usually requires a downpayment as little is 3-3.5%, but investment properties require 20% down (there are practically no exceptions). So, for a $200,000 house, the down payment for an investment property would be $40,000 as opposed to only $7000 for a primary residence. This makes purchasing rental properties- without them first being primary residences- out of reach for many homeowners, even if their income is sufficient to support the mortgage payment for 2 properties.

The Workaround

If you have grown children (even ones that don’t seem to provide much “return on investment”!) then it is likely you could “use” them to pick up a rental property for only 3.5% down, making such an investment far more achievable for some people.

Here’s how it works:

FHA mortgages (and now conventional mortgages) allow for “non-occupying co-borrowers”, as long as they are related. That means you can be an owner/borrower of/on a property without actually living there, as long as a family member is living in the home as their primary residence. Underwriters would consider the combined income, assets, debt payments, etc. of all borrowers when approving the loan, but it’s perfectly acceptable to have practically all of the income coming from you (the parents). The occupying borrower would need to plan on living there for at least a year, but after that, it’s completely acceptable to treat the property as a rental.

Application of this Strategy

This is an exceptionally good strategy for parents with children attending college or children that are planning on renting anyway. Here is an example of how this often works (I’m using actual expected mortgage payments and rental rates, based off the current Utah County market):

Example 1: Mom & Dad buy a condo close to campus for $150,000 and put down 3.5% ($5250). The mortgage payment (with taxes and insurance) and HOA fee come to $987/month. Jimmy (the son) and his 2 roommates live there, with the 2 roommates paying $350/month in rent (they give Jimmy a break and only charge him $287). The parents pay nothing (unless they were going to pay Jimmy’s rent anyway) while Jimmy finishes school. Jimmy finishes school 3 years later and Mom & Dad then refinance the loan into a conventional loan without mortgage insurance (which they can now do, since the home has appreciated and they’ve paid down the mortgage), yielding a new payment of $900/month. They could rent the property to 3 students for $1050/month and still net $100/month, even after reserving for maintenance.

That $100 may not seem like a lot, but keep in mind that the mortgage is being paid down and the property is appreciating. By the time Mom & Dad are ready to retire, they would have a substantial amount of equity (close to $150,000, after 15 years).

Example 2: Jimmy (from our previous example) gets married, has a few kids, and moves to a new city. It will be a year or 2 before they can buy a house themselves and renting a $200,000 home (the size required for their family size) will cost about $1300/month. Mom & Dad figure out that buying the same house (as non-occupying co-borrowers putting down just 3.5%) would yield a total mortgage payment of only $1192. They decide to buy the house with Jimmy and his wife and let them pay $1200 in rent. Jimmy and family get a break on rent and Mom & Dad just picked up a rental for only $7000 down!

A lot goes into purchasing rentals and managing them, but the returns are substantial, if done correctly (see our blogpost about rentals here). If you’ve been considering acquiring a (or additional) rental(s) and have some grown kids to “cash in”, give us a call. We’ll do a complete analysis so that you can see if it would work for you and your family.

Rate post 6/1/2016

Why You Shouldn’t Wait Until You Have a 20% Down Payment

It’s surprising how many mortgage and financial professionals are still advocating a 20% down payment. It’s bad advice and lazy thinking, as we’ll make clear.

The Old Argument: Don’t buy a home unless you can put down 20%

It’s true that putting down 20% will shield you from mortgage insurance most of the time (some loans will still require mortgage insurance). Also, the mortgage will be smaller (since you put more down), so the mortgage payment will be smaller.

But most people don’t have 20% to put down. Not even close. That is a $40,000 down payment for a $200,000 home (which is considered “small” in Utah and Salt Lake Counties).

The Better Argument: Delaying homeownership until you have a 20% down payment is a waste of time and money

The crux of this argument is Net Worth, at least as it relates to housing. The non-technical definition of net worth is how much cash you would have if you sold all of your assets and paid off all of the associated debts. Let’s compare the net worth of two couples, one who put down 3.5% and bought a home now (we’ll call them the Flanders) and a couple that waited until they had a 20% down payment (we’ll call them the Wiggums).

First, a few assumptions:

Both couples want/need a $200,000 home.

The cost of renting is roughly equal to a mortgage payment for the same home (this is true, in today’s market).

Homes in Utah appreciate 5% per year (a conservative average for the last 5 years).

Both couples have $7500 saved now and can/will save another $6500 per year for the next 5 years.

The Flanders (3.5% down) –

The Flanders have enough to put down 3.5% on a $200,000 home right now ($7500). They buy the home and live in it for 5 years.

After 5 years, the mortgage balance is down to about $175,000 and the home is worth about $255,000.

They sell the home, pay off the mortgage, and walk with $80,000.

They’ve also saved $6500/year for the last 5 years, giving them another $32,500. The Flanders’ net worth is $112,500.

The Wiggums (20% down) –

The Wiggums can’t put down 20% now (and won’t be convinced otherwise), so they save for 5 years, renting the entire time.

After 5 years, they buy a home, putting down $40,000. For comparison’s sake, they sell the home the next month.

Their mortgage balance is $160,000 and the home is worth about $200,000 (they just bought it), so they walk with $40,000.

The $6500/year they saved went towards the down payment, so the Wiggums net worth is just $40,000.

Each couple spent the same amount for housing, savings, etc., but the Flanders have almost $80,000 more than the Wiggums. Plus, since the Wiggums waited 5 years to buy a home, rates would likely be higher and the home that cost $200,000 at first now costs $255,000 (because of 5% annual appreciation)!

There are exceptions that could affect this analysis (sudden market crash, super cheap rent compared to mortgage payments), but even accounting for those, it is almost always better to buy as soon as it is feasible.

There are few no-brainers in the financial world. This is one of them. It makes NO sense to forego homeownership until you have a 20% down payment!

For more information, feel free to look here.

A few tips toward adding value to your home (and a few things to avoid)

Whether you are selling, refinancing, or just renting, upgrading certain aspects of your home can be a boon toward raising it’s value, while others are just a money-sink with no real return. Here at Evergreen Mortgage, we took a look at some of the best (and worst) places to sink time, money, and effort into to get the best bang for your buck.

Image by Nancy Hugo, CKD

1.Remodeling your kitchen.

It is a well-known fact that the kitchen is among the most important rooms in the home. You will definitely want this looking nice before getting that appraisal.

Replacing outdated appliances, and repairing or replacing the counters or floors, if needed, will go a long way toward making your home feel modern and up-to-date. Try spending money on stainless steel appliances for that truly modern look and feel.

Also, adding a fresh coat of paint never hurts either. Upgrading the kitchen can even raise the value of your home between 3%-7% on average.

Photo of a finished basement by Sean Madden. License Labelled for Reuse

2. Finish your basement or attic.

Not only will this add usable square footage to your home, but allows for a flexible living space, that can serve a variety of purposes: an extra room, an office, a second living room, a playroom for the kids, or the adults, the possibilities are endless.

The bottom line is having the extra usable space never hurts. Doing this can raise the value of the home between 4%-6% on average.

Image by Todtanis

3. Freshen up the bathrooms.

Just like the kitchen, bathrooms should feel fresh and updated. Replacing your worn out linoleum floor, or possibly simply the faucets and fixtures, can go a long way toward improving the overall value of the home. You don’t have to go overboard, make the bathroom look nice. No one wants an old messy bathroom.

Some other things to consider:

Re-painting rooms that need it is an easy, cost effective way to add value to your home.

Update all of your energy-guzzling appliances to make your home energy efficient, replace single-pane windows with double-pane or triple-pane windows. For better heat retention and energy efficiency.

Maintain and fix any leaky faucets or drains, replace burnt out bulbs, and make sure the home is clean and presentable.

Doing these three things, is practically guaranteed to get some value, but let’s look at some of the things that won’t.

Image by Vic Brincat From Ontario Canada

1. Installing a pool.

While it is wonderful to be able to cool off during the summer time, adding a pool likely isn’t likely to raise the value of your home. That doesn't mean you shouldn't make the investment if you want a pool, just be aware that with maintenance costs it is more a liability than an asset. Whether you are simply refinancing, or trying to sell your home, a pool is an investment best left to those who really want one.

Image by Todtanis

2. Creating specialized spaces. While you may have always wanted to convert that bedroom into a personal sauna, it might not work out so well when it comes time to sell or refinance. Individuals looking at your home on Zillow or other websites will expect a certain number of rooms to be present. If the house no longer fits the description, they may look elsewhere.

Long story short, sometimes it is best to keep things simple.

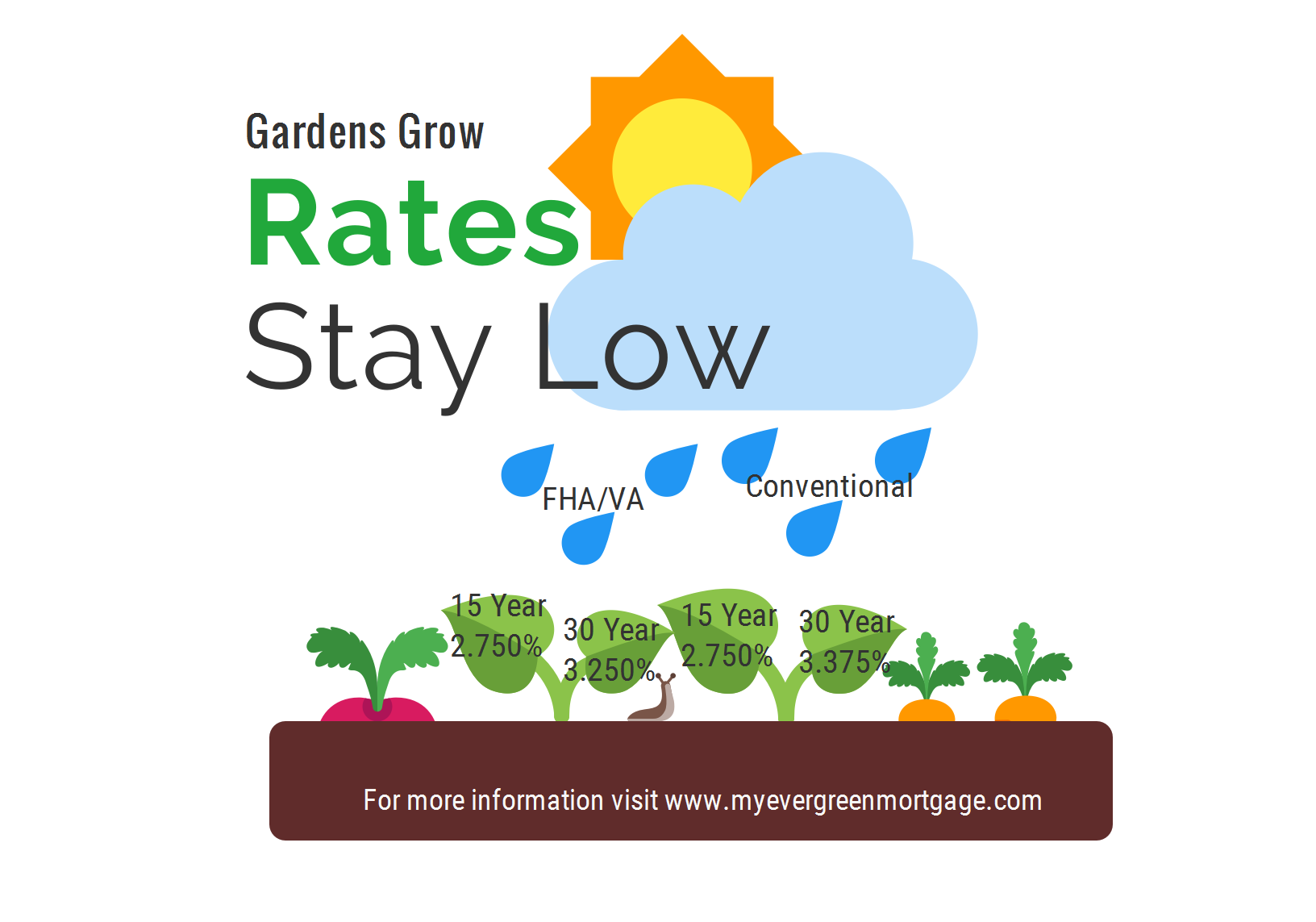

Rate Post 5/9/2016

Slight rise in interest rates

Interest rates have gone up ever so slightly this month, but are still pretty low.

Recent Home Value Changes: Utah vs. Everyone Else

Most everyone agrees that the real estate “rebound” is in full swing, and has been for some time. But, as the experts say, real estate is local, and just as the bust affected each region differently, so has the rebound.

The chart below represents how home prices have changed over the last 3 years, comparing Utah to the rest of the country.

What does this mean?

Here are several takeaways from this information:

· Nationally, rates of home appreciation have returned to close to normal – The 100-yr average of real estate appreciation is 3.5%. The country is currently just under 4%, and while some areas are still exploding (parts of California, Florida, etc.), overall, things have “calmed down”.

· Utah is still charging hard – Utah is experiencing real growth (people are moving to the state and those that are here are having kids!). There is a real demand for housing and that demand continues to drive up the price of real estate.

· What happened in 2014? – The drop in home values in 2014 is surprising. This could be due to a simple correction (of overly-optimistic pricing in previous years), timing of new homes being built, etc. Most importantly, though real estate tends to increase in value, it’s not an unwavering trend (and this is just a 3-yr sample).

Not all of Utah is created equal

As a further example of real estate is local, below is the same chart, comparing just Salt Lake City, Provo, and Ogden:

Key Takeaways:

· Along the Wasatch Front, Utah County continues to outpace other counties – Though the rate of growth has evened out, Utah county continues to be a hotbed for tech companies and other startups.

· Salt Lake faltered, but came roaring back – With almost a 9% drop in home values in 2014, Salt Lake saw the steepest rebound in 2015, proof that the most populated city is still a favored destination.

· Ogden is the least volatile – Home prices remain affordable, even though Ogden has had the highest average 3-yr rate of growth amongst these 3 cities.

In a nutshell:

Utah’s true growth makes its real estate a solid long-term investment. But, that also means that if you’re thinking about buying, homes will likely be 7% more expensive a year from now, so act fast (if prudent)!